The Evolution of Personal Finance since 1922

Significant Transformations in Personal Finance

Over the past century, personal finance has undergone significant transformations. The landscape has shifted due to changes in economic conditions, technological advancements, and evolving consumer behaviors. Understanding these shifts is essential for effectively managing finances in today’s fast-paced world.

Key Milestones in the Evolution of Personal Finance

Several critical events have shaped personal finance, affecting how consumers manage their money and access financial services:

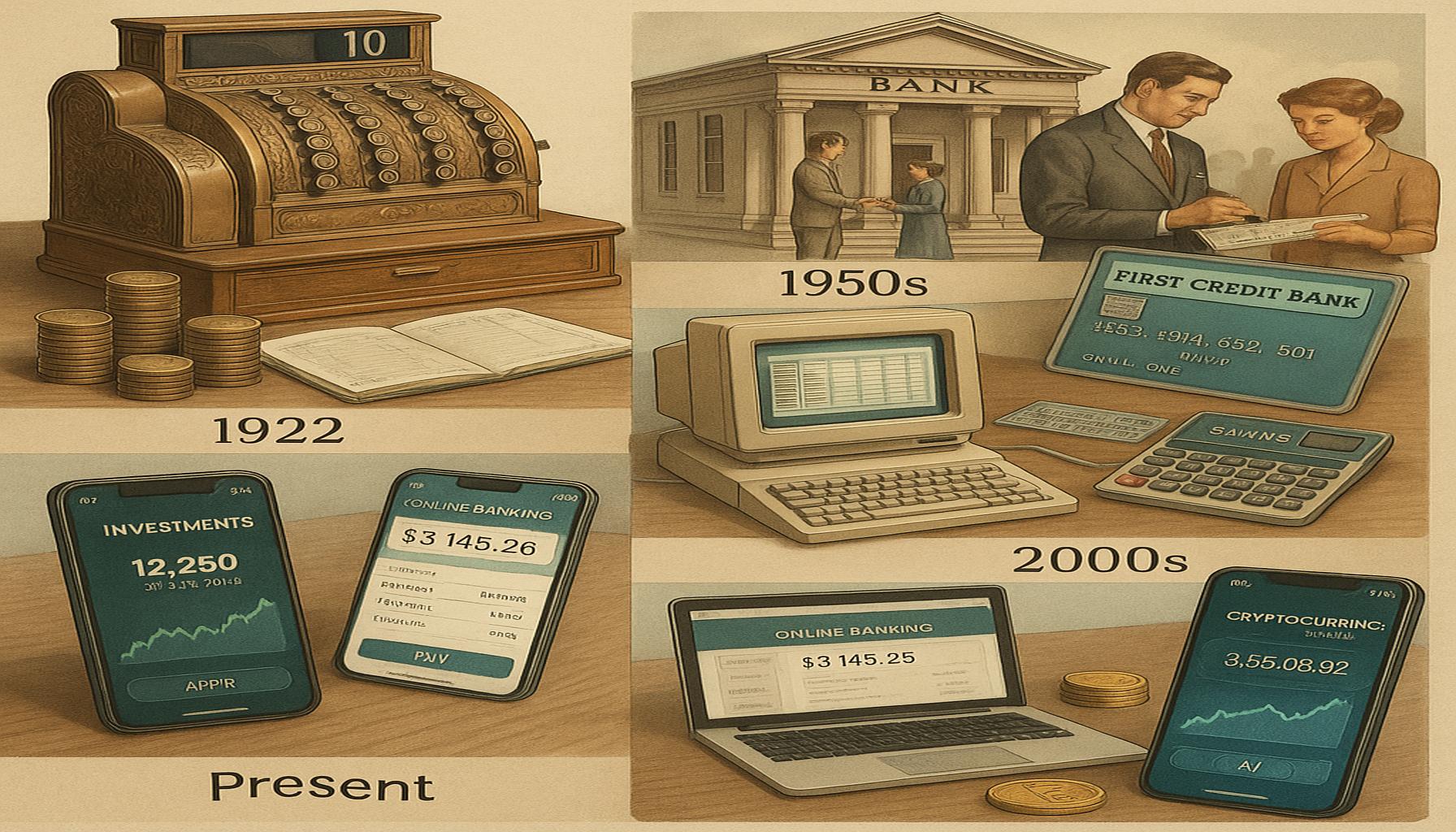

- The Great Depression (1930s) – This economic crisis highlighted the necessity for savings and risk management. Many families learned the hard way about financial instability, prompting a shift toward saving for emergencies. The introduction of the Federal Deposit Insurance Corporation (FDIC) in 1933 restored trust in the banking system by insuring deposits, which helped lay the foundation for modern savings habits.

- The Introduction of Credit Cards (1950s) – Credit cards revolutionized consumer spending and borrowing. The advent of the General Motors Acceptance Corporation (GMAC) credit card in 1950 began a new era of convenience. Consumers could purchase items and pay for them over time, leading to increased consumerism, but also necessitating a better understanding of debt management. Today, it’s essential for cardholders to track their expenses and stay within their budget to avoid high-interest rates and debt accumulation.

- Online Banking (1990s) – The rise of the internet brought banking to consumers’ fingertips, allowing for real-time account access and management. With online banking services, users can view balances, transfer funds, and pay bills from the comfort of their homes. This shift not only increased convenience but also encouraged diligent financial oversight.

- The Rise of Financial Technology (Fintech) (2000s) – The emergence of fintech companies has transformed personal finance by providing innovative solutions for budgeting, investing, and personal finance management. Services like PayPal, Mint, and Robinhood have made it easier than ever for individuals to manage their finances, invest, and track their spending.

Essential Tools and Resources

Today, individuals have access to an abundance of tools and resources to take control of their financial futures. Some essential features include:

- Mobile Apps – These applications enable users to track spending in real-time, set budgets, and receive alerts for upcoming bills. Popular options include YNAB (You Need A Budget) and Personal Capital, which help users identify spending patterns and save effectively.

- Robo-Advisors – Platforms like Betterment and Wealthfront offer automated investment management through algorithms, allowing users to invest without the need for extensive knowledge of financial markets. These services typically provide low fees, making investing more accessible.

- Online Courses and Blogs – Access to education on financial literacy is more prevalent than ever, with numerous courses and blogs dedicated to topics such as saving, investing, and retirement planning. By taking advantage of resources from websites like Coursera or financial blogs, individuals can empower themselves to make informed decisions.

Understanding these changes is vital for making informed financial decisions today. By grasping the evolution of personal finance, you can better navigate current challenges and effectively plan for the future. Taking proactive steps—such as utilizing the latest technology and continuously educating yourself—will build a stronger financial foundation for you and your family.

DISCOVER MORE: Click here to learn about the impact of 5G on financial services

Transformative Effects of Historical Events on Personal Finance

The trajectory of personal finance has not only been shaped by technological advancements but also by significant historical events that altered consumer behavior and financial management practices. Here’s a closer look at how these pivotal moments have influenced the way individuals handle their finances:

The Great Depression and Its Aftermath

The Great Depression in the 1930s was a watershed moment for personal finance. As millions faced unemployment and financial ruin, people recognized the importance of financial security. Savings became a priority for many families, and the concept of emergency funds entered the collective consciousness. The establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 was crucial in restoring confidence in the banking system, ensuring that deposits were protected. This led to a culture of saving and prudent financial management that persists today.

The Role of Credit in the Mid-20th Century

The introduction of credit cards in the 1950s marked a critical turning point in consumer finance. Initially launched by the General Motors Acceptance Corporation (GMAC), credit cards offered consumers convenience and flexibility in making purchases. However, this new financial tool also required individuals to develop skills in debt management. The ability to repay borrowed funds, track expenses, and maintain a good credit score became essential for responsible credit use. Consumers quickly learned that while credit could enhance purchasing power, mismanagement could lead to crippling debt.

The Digital Transformation in the 1990s

The rise of the internet in the 1990s forever changed personal finance through the advent of online banking. For the first time, customers could manage their accounts and conduct transactions from the comfort of their homes. This accessibility enabled users to monitor their finances closely and respond quickly to changes. With online tools, individuals could pay bills, transfer funds, and check balances in real-time, leading to enhanced financial accountability.

The Financial Technology Revolution

Since the 2000s, the emergence of financial technology (fintech) has transformed the financial landscape further. Fintech solutions have made financial services more affordable and accessible. Tools like budgeting apps, investment platforms, and personal finance software have democratized finance, allowing more people to take control of their financial futures. Services such as PayPal facilitate online shopping, while applications like Mint help users track expenses and manage budgets on-the-go.

For those looking to navigate the modern financial landscape, leveraging these technological advancements is vital. Embrace the tools available to you, and keep in mind the lessons learned from historical events. A proactive approach to personal finance—one that includes savings practices, responsible credit card usage, and an understanding of digital finance—will position individuals for success. Engaging with the evolving financial environment can lead to informed decision-making and long-term prosperity.

DIVE DEEPER: Click here to discover more about genomics and health

The Impact of Regulatory Changes and Economic Trends

As personal finance continued to evolve, changes in regulations and economic trends played a vital role in shaping consumer behavior. Understanding these factors can provide valuable insight into how individuals manage their financial lives today.

The Rise of Financial Regulations

In the wake of the stock market crash of 1929 and subsequent financial crises, the U.S. government implemented a series of regulatory reforms aimed at protecting consumers and stabilizing the economy. The Securities Exchange Act of 1934 established the Securities and Exchange Commission (SEC) to oversee and regulate the securities industry. This development fostered transparency and accountability, helping individuals feel more secure when investing in stocks and bonds. Awareness of financial regulations encouraged consumers to educate themselves on investment opportunities and risks, leading to a more financially literate populace.

The Inflationary Era and Its Consequences

The 1970s were marked by rampant inflation, significantly impacting personal finance strategies. As prices soared, traditional savings accounts yielded little to no interest, prompting individuals to seek higher returns through investments in equities or real assets such as real estate. Inflation protection became a priority, and many turned to instruments like Treasury Inflation-Protected Securities (TIPS) to safeguard their purchasing power. As a result, diversified investment strategies began to take shape, teaching consumers the importance of asset allocation and risk management.

The Emergence of Investment Accounts

In the 1980s and 1990s, the introduction of 401(k) plans revolutionized retirement savings. Employers began offering these tax-advantaged accounts to incentivize their workforce to save for retirement. Workers now had the responsibility to manage their contributions, reinforcing the need for personal financial planning. This shift away from traditional pensions forced individuals to educate themselves on investment strategies, risk tolerance, and long-term financial goals. As a result, retirement planning became a crucial aspect of personal finance, leading to a new generation of financially aware individuals.

The Great Recession and an Increased Awareness of Risk

The financial crisis of 2008 underscored the significance of understanding risk and maintaining financial stability. Poor lending practices and lack of oversight led to widespread job loss, diminished home values, and failures of major financial institutions. In the aftermath, Americans became more mindful of their spending habits and credit use. Enhanced scrutiny on large financial institutions spurred regulatory reforms, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act, which aimed to protect consumers and prevent future crises. Individuals learned the importance of diversifying investments and avoiding excessive debt, helping foster a more risk-averse financial environment.

The Current Era of Fintech and Financial Independence

Today, the landscape of personal finance is shaped by a culture of self-reliance powered by technology. The rise of robo-advisors and online investment platforms empowers investors with limited capital to participate in the stock market. Likewise, mobile payment services like Venmo and Cash App enhance the convenience of personal transactions. As access to information increases, consumers can easily compare financial products, allowing them to make informed choices that best suit their needs.

Individuals today must navigate a more complex financial world that emphasizes self-sufficiency, responsible debt management, and strategic investment. Embracing the lessons of past economic shifts and regulatory changes can serve as a foundation for building a robust personal finance strategy in the present and future.

DISCOVER MORE: Click here to learn about the Emirates Skywards World Elite Mastercard</p

Conclusion

The journey of personal finance from 1922 to the present day reflects significant changes driven by regulatory shifts, economic realities, and technological advancements. Understanding these historical milestones is paramount for anyone aiming to navigate today’s complex financial landscape. Regulations established in response to economic crises have ensured enhanced consumer protection and transparency, allowing individuals to engage more confidently in investment opportunities.

Furthermore, the crises of the past, particularly the inflationary pressures of the 1970s and the 2008 financial collapse, emphasized the importance of risk management and financial literacy. These events have taught consumers the necessity of diversification and conscious spending practices. Today, with the rise of fintech solutions, individuals have access to an array of tools that facilitate better financial decisions, from automated savings to investment platforms.

To effectively manage personal finances in the current environment, it is crucial to take specific steps:

- Stay informed about regulatory changes that impact consumer finance.

- Develop a diversified investment portfolio that aligns with your risk tolerance and long-term goals.

- Utilize available financial technologies to track expenses, savings, and investments.

- Commit to ongoing education in personal finance to adapt to both personal circumstances and broader economic trends.

By applying these principles and leveraging available resources, individuals can build a solid financial future that not only honors the lessons of the past but also embraces the opportunities of the present and future. In a world where financial independence is increasingly attainable, proactive engagement with one’s financial well-being remains the key to success.

Linda Carter is a financial writer and consultant with expertise in economics, personal finance, and investment strategies. With years of experience helping individuals and businesses navigate complex financial decisions, Linda provides practical insights and analysis on. His goal is to empower readers with the knowledge they need to achieve financial success.